In December 2020, Congress passed the Corporate Transparency Act (CTA) as part of the National Defense Authorization Act. According to the Financial Crimes Enforcement Network (FinCEN), the purpose of the CTA is to “better enable critical national security, intelligence, and law enforcement efforts to counter money laundering, the financing of terrorism, and other illicit activity “by creating a federal framework for reporting, storing, and disclosing beneficial ownership information of “reporting companies.”

While the CTA was ostensibly targeted to foreign- owned companies, domestic companies- particularly small businesses- who meet the broad definition of reporting company will be affected by the CTA’s disclosure provision. The CTA takes effect on Jan. 1, 2024 – and companies should consider preparing now.

The following is taken from instructions for the BOI Report. This should provide generall information concerning filing requirements. We have included, as well, a definition of a beneficial owner at the end of this blog.

We have also included the actual report for your reference.

A. General Questions

A. 1. What is beneficial ownership information?

Beneficial ownership information refers to identifying information about the individuals who directly or indirectly own or control a company.

[Issued March 24, 2023]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

A. 2. Why do companies have to report beneficial ownership information to the U.S. Department of the Treasury?

In 2021, Congress passed the Corporate Transparency Act on a bipartisan basis. This law creates a new beneficial ownership information reporting requirement as part of the U.S. government’s efforts to make it harder for bad actors to hide or benefit from their ill-gotten gains through shell companies or other opaque ownership structures.

[Issued September 18, 2023]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

A. 3. Under the Corporate Transparency Act, who can access beneficial ownership information?

FinCEN will permit Federal, State, local, and Tribal officials, as well as certain foreign officials who submit a request through a U.S. Federal government agency, to obtain beneficial ownership information for authorized activities related to national security, intelligence, and law enforcement. Financial institutions will have access to beneficial ownership information in certain circumstances, with the consent of the reporting company. Those financial institutions’ regulators will also have access to beneficial ownership information when they supervise the financial institutions.

FinCEN published the rule that will govern access to and protection of beneficial ownership information on December 22, 2023. Beneficial ownership information reported to FinCEN will be stored in a secure, non-public database using rigorous information security methods and controls typically used in the Federal government to protect non-classified yet sensitive information systems at the highest security level. FinCEN will work closely with those authorized to access beneficial ownership information to ensure that they understand their roles and responsibilities in using the reported information only for authorized purposes and handling in a way that protects its security and confidentiality.

[Updated January 4, 2024]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

A. 4. How will companies become aware of the BOI reporting requirements?

FinCEN is engaged in a robust outreach and education campaign to raise awareness of and help reporting companies understand the new reporting requirements. That campaign involves virtual and in-person outreach events and comprehensive guidance in a variety of formats and languages, including multimedia content and the Small Entity Compliance Guide (https://www.fincen.gov/boi/small-entity-compliance-guide) , as well as new channels of communication, including social media platforms. FinCEN is also engaging with governmental offices at the federal and state levels, small business and trade associations, and interest groups.

FinCEN will continue to provide guidance, information, and updates related to the BOI reporting requirements on its BOI webpage, www.fincen.gov/boi. Subscribe here (https://service.govdelivery.com/accounts/USFINCEN/subscriber/new) to receive updates via email from FinCEN about BOI reporting obligations.

[Issued December 12, 2023]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

B. Reporting Process

B. 1. Should my company report beneficial ownership information now?

FinCEN launched the BOI E-Filing website for reporting beneficial ownership information (https://boiefiling.fincen.gov) on January 1, 2024.

* A reporting company created or registered to do business before January 1, 2024, will have until January 1, 2025, to file its initial BOI report.

* A reporting company created or registered in 2024 will have 90 calendar days to file after receiving actual or public notice that its creation or registration is effective.

* A reporting company created or registered on or after January 1, 2025, will have 30 calendar days to file after receiving actual or public notice that its creation or registration is effective.

[Updated January 4, 2024]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

B. 2. When do I need to report my company’s beneficial ownership information to FinCEN?

A reporting company created or registered to do business before January 1, 2024, will have until January 1, 2025 to file its initial beneficial ownership information report.

A reporting company created or registered on or after January 1, 2024, and before January 1, 2025, will have 90 calendar days after receiving notice of the company’s creation or registration to file its initial BOI report. This 90-calendar day deadline runs from the time the company receives actual notice that its creation or registration is effective, or after a secretary of state or similar office first provides public notice of its creation or registration, whichever is earlier.

Reporting companies created or registered on or after January 1, 2025, will have 30 calendar days from actual or public notice that the company’s creation or registration is effective to file their initial BOI reports with FinCEN.

[Updated December 1, 2023]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

B. 3. When will FinCEN accept beneficial ownership information reports?

FinCEN will begin accepting beneficial ownership information reports on January 1, 2024. Beneficial ownership information reports will not be accepted before then.

[Issued March 24, 2023]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

B. 4. Will there be a fee for submitting a beneficial ownership information report to FinCEN?

No. There is no fee for submitting your beneficial ownership information report to FinCEN.

[Updated January 4, 2024]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

B. 5. How will I report my company’s beneficial ownership information?

If you are required to report your company’s beneficial ownership information to FinCEN, you will do so electronically through a secure filing system available via FinCEN’s BOI E-Filing website (https://boiefiling.fincen.gov).

[Updated January 4, 2024]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

B. 6. Where can I find the form to report?

Access the form by going to FinCEN’s BOI E-Filing website (https://boiefiling.fincen.gov) and select “File BOIR.”

[Updated January 4, 2024]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

B. 7. Is a reporting company required to use an attorney or a certified public accountant (CPA) to submit beneficial ownership information to FinCEN?

No. FinCEN expects that many, if not most, reporting companies will be able to submit their beneficial ownership information to FinCEN on their own using the guidance (https://www.fincen.gov/boi/small-business-resources) FinCEN has issued. Reporting companies that need help meeting their reporting obligations can consult with professional service providers such as lawyers or accountants.

[Issued November 16, 2023]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

B. 8. Who can file a BOI report on behalf of a reporting company, and what information will be collected on filers?

Anyone whom the reporting company authorizes to act on its behalf—such as an employee, owner, or third-party service provider—may file a BOI report on the reporting company’s behalf. When submitting the BOI report, individual filers should be prepared to provide basic contact information about themselves, including their name and email address or phone number.

[Issued December 12, 2023]

Back to top (https://www.fincen.gov/boi-faqs#Top_section)

C. Reporting Company

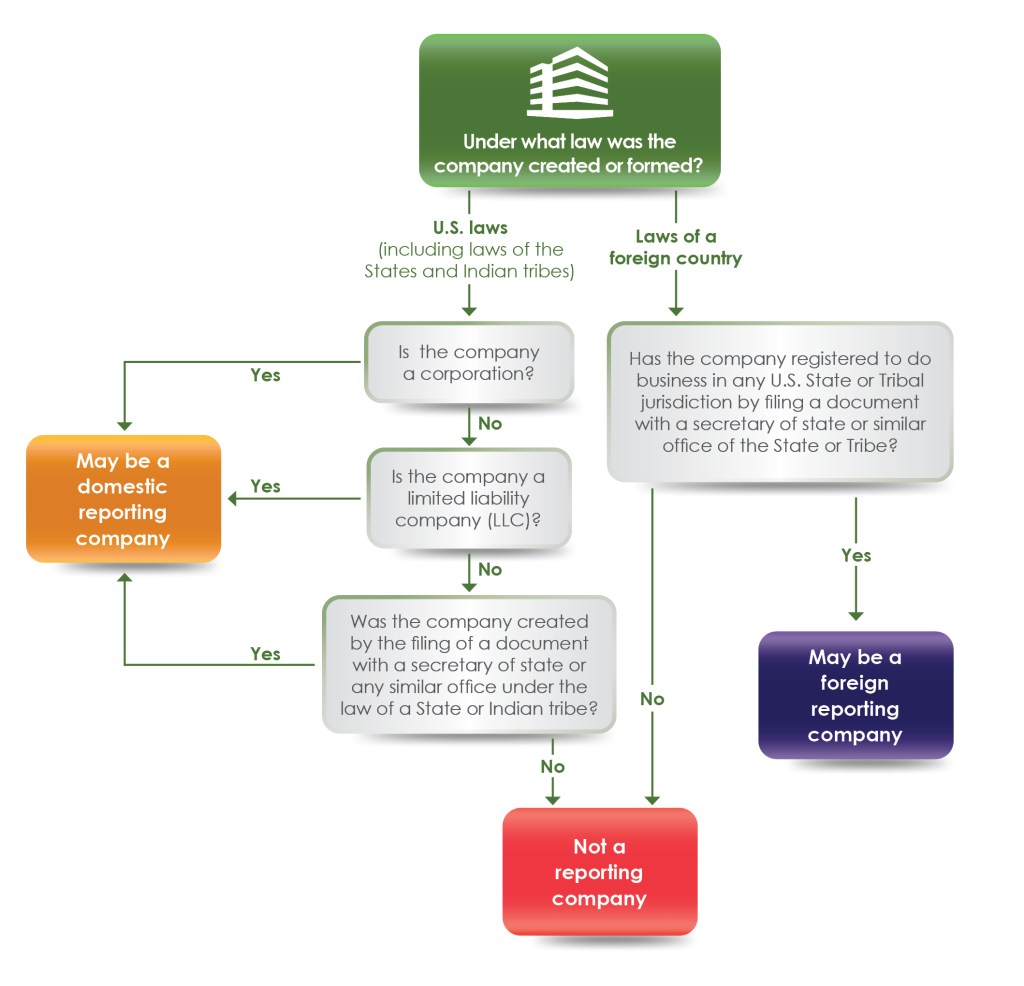

C. 1. What companies will be required to report beneficial ownership information to FinCEN?

Companies required to report are called reporting companies. There are two types of reporting companies:

* Domestic reporting companies are corporations, limited liability companies, and any other entities created by the filing of a document with a secretary of state or any similar office in the United States.

* Foreign reporting companies are entities (including corporations and limited liability companies) formed under the law of a foreign country that have registered to do business in the United States by the filing of a document with a secretary of state or any similar office.

There are 23 types of entities that are exempt from the reporting requirements (see Question C.2). Carefully review the qualifying criteria before concluding that your company is exempt.

FinCEN’s Small Entity Compliance Guide (https://www.fincen.gov/boi/small-entity-compliance-guide) for beneficial ownership information reporting includes the following flowchart to help identify if a company is a reporting company (see Chapter 1.1, “Is my company a “reporting company”?”).

2. Are some companies exempt from the reporting requirement?

Yes, 23 types of entities are exempt from the beneficial ownership information reporting requirements. These entities include publicly traded companies meeting specified requirements, many nonprofits, and certain large operating companies.

The following table summarizes the 23 exemptions:

Exemption No. Exemption Short Title

1 Securities reporting issuer

2 Governmental authority

3 Bank

4 Credit union

5 Depository institution holding company

6 Money services business

7 Broker or dealer in securities

8 Securities exchange or clearing agency

9 Other Exchange Act registered entity

10 Investment company or investment adviser

11 Venture capital fund adviser

12 Insurance company

13 State-licensed insurance producer

14 Commodity Exchange Act registered entity

15 Accounting firm

16 Public utility

17 Financial market utility

18 Pooled investment vehicle

19 Tax-exempt entity

20 Entity assisting a tax-exempt entity

21 Large operating company

22 Subsidiary of certain exempt entities

23 Inactive entity

Beneficial owners

A “beneficial owner” includes any individual who, directly or indirectly, exercises substantial control over a reporting company. An individual exercises “substantial control” over a reporting company if the individual meets any of four general criteria:

1) The individual is a senior officer

2) The individual has authority to appoint or remove certain officers or a majority of directors of the reporting company

3) The individual is an important decision-maker

4) The individual has any other form of substantial control over the reporting company

No ownership interest in the reporting company is required. There is also no limit on the number of individuals who may be treated as exercising substantial control over a reporting company. An individual can exercise substantial control, directly or indirectly, over a reporting company, including through contracts, arrangements, understandings, intermediary entities or other relationships.

A “beneficial owner” also includes any individual who, directly or indirectly, owns or controls at least 25% of the ownership interests of a reporting company. A reporting company may have multiple types of ownership interests. Examples of ownership interests include equity, stock, or voting rights, a capital or profit interest, convertible instruments, options or other non-binding privileges to buy or sell any of the foregoing, and any other instrument, contract, or mechanism used to establish ownership.